About Chiheb Ben Hammouda Chiheb Ben Hammouda Ph.D., Applied Mathematics and Computational Science Numerical simulation and analysis Quantitative finance Computational biology Stochastic Modeling Chiheb Ben Hammouda is a Ph.D. candidate at Stochastic Numerics Research Group (STOCHNUM) under the supervision of Professor Raul F. Tempone at King Abdullah University of Science and Technology (KAUST). Prior to joining Ph.D., Chiheb obtained a Master's degree in Applied Mathematics and Computational Sciences from KAUST, and a Bachelor's degree in multidisciplinary engineering from Ecole Polytechnique de Tunisie, Tunisia. Research Interests Chiheb's research interests include Stochastic modeling, Numerical simulation and analysis, Quantitative finance in particular option pricing, Stochastic Articles Related News May 2026 Preprint in Mathematical Finance from our research team 2 min read · Mon, May 18 2026 News The Stochastic Numerics Group would like to highlight the recent achievement within our research group. On the 30th of April, “Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers” was published on arXiv. The authors of this paper are Assistant Professor Chiheb Ben Hammouda of Utrecht University, PhD student Michael Samet of RWTH, and PI Raul Tempone. We would like to congratulate these authors on the preprint of their paper. Our research develops a data-driven continuous-time stochastic optimal control framework for intraday electricity trading by November 2022 New publication in Quantitative Finance Journal 1 min read · Wed, Nov 2 2022 News Adaptive sparse grid quadrature Quasi-Monte Carlo Numerical smoothing Richardson extrapolation option pricing Monte Carlo Distribution functions Greeks Risk estimation At the end of October, the paper Numerical smoothing with hierarchical adaptive sparse grids and quasi-Monte Carlo methods for efficient option pricing by Christian Bayer ( Weierstrass Institute for Applied Analysis and Stochastics - WIAS) , Chiheb Ben Hammouda ( RWTH Aachen University ) , and Raul Tempone ( King Abdullah University of Science and Technology - KAUST; RWTH Aachen University ), was published in the Quantitative Finance Journal and is available at Taylor & Francis Online. Abstract: When approximating the expectations of a functional of a solution to a stochastic differential August 2022 Ph.D. student Eliza Rezvanova visited RWTH Aachen University 1 min read · Sun, Aug 28 2022 News During two weeks in August 2022, Ph.D. student Eliza Rezvanova visited RWTH Aachen University to collaborate with Dr. Chiheb Ben Hammouda on stochastic optimal control of renewable energy project. August 2020 A talk by Dr. Chiheb Ben Hammouda in the Monte Carlo & Quasi-Monte Carlo (MCQMC) Methods in Scientific Computing Conference, in August 2020, University of Oxford 1 min read · Tue, Aug 11 2020 News Monte Carlo markov chains Dr. Chiheb Ben Hammouda gave, on August 11, 2020, a talk entitled "Importance sampling for a robust and efficient multilevel Monte Carlo estimator for stochastic reaction networks" in the Monte Carlo & Quasi-Monte Carlo (MCQMC) Methods in Scientific Computing Conference, 10-14 August 2020, University of Oxford. Prof. Raul Tempone and Dr. Chiheb Ben Hammouda are organizing a minisymposia "Hierarchical Methods for Variance Reduction" at the MCQMC Conference, 10-14 August 2020, University of Oxford 1 min read · Mon, Aug 3 2020 News Monte carlo methods Prof. Raul Tempone and Dr. Chiheb Ben Hammouda are organizing a mini-symposia "Hierarchical Methods for Variance Reduction" at the Monte Carlo & Quasi-Monte Carlo Methods in Scientific Computing Conference, 10-14 August 2020, University of Oxford. July 2020 Chiheb Ben Hammouda succesfully defended his PhD Thesis 2 min read · Thu, Jul 2 2020 News On July 2nd, 2020, Chiheb Ben Hammouda successfully defended his Ph.D. thesis entitled "Hierarchical Approximation Methods for Option Pricing and Stochastic Reaction Networks" June 2020 PhD Thesis Defense: Hierarchical Approximation Methods for Option Pricing and Stochastic Reaction Networks by Chiheb Ben Hammouda 3 min read · Sun, Jun 21 2020 News In biochemically reactive systems with small copy numbers of one or more reactant molecules, stochastic effects dominate the dynamics. In the first part of this thesis, we design novel efficient simulation techniques for a reliable and robust estimation of various statistical quantities for stochastic biological and chemical systems under the framework of Stochastic Reaction Networks (SRNs). February 2020 A series of seminar talks at RWTH Aachen University (Germany) by Chiheb Ben Hammouda 1 min read · Mon, Feb 10 2020 News Chiheb Ben Hammouda will give a series of seminar talks at RWTH Aachen University (Germany) between 14 and 27 February. The talks will be related to the following manuscripts Bayer, Christian, Chiheb Ben Hammouda, and Raul Tempone. "Hierarchical adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model." Quantitative Finance Journal (2020), DOI: 10.1080/14697688.2020.1744700. August 2019 KAUST Ph.D. student wins Society for Industrial and Applied Mathematics award 2 min read · Wed, Aug 21 2019 News Spotlight Stochastic Modeling Quantitative finance Numerical simulation and analysis Chiheb Ben Hammouda, a KAUST Ph.D. student in the University's Stochastic Numerics Research Group, recently won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) held at the University of Toronto from June 4 to 7. His winning poster, titled "Hierarchical adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model," is one of several research projects carried out by Ben Hammouda under the supervision of KAUST Professor Raul Tempone. July 2019 A talk by Chiheb Ben Hammouda in the International Conference on Computational Finance 2019 (ICCF2019), Coruña, Spain 1 min read · Mon, Jul 1 2019 News Chiheb Ben Hammouda will give, on July 12, 2019, a talk entitled "Adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model" at the International Conference on Computational Finance 2019 (ICCF2019), Coruña, Spain. June 2019 Chiheb Ben Hammouda won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) 1 min read · Thu, Jun 6 2019 News Chiheb Ben Hammouda won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) held at the University of Toronto from June 4 to 7, 2019. May 2015 Chiheb Ben Hammouda successfully defended his MS Thesis 2 min read · Mon, May 4 2015 News On April 30th, 2015, Chiheb Ben Hammouda successfully defended his MS Thesis entitled "Drift-Implicit Multi-Level Monte Carlo Tau-Leap Methods for Stochastic Reaction Networks".

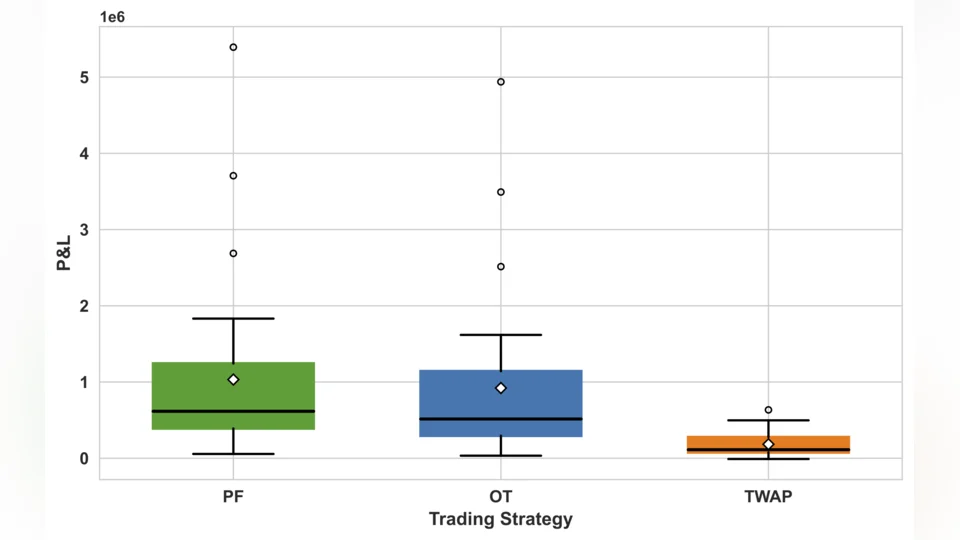

Preprint in Mathematical Finance from our research team 2 min read · Mon, May 18 2026 News The Stochastic Numerics Group would like to highlight the recent achievement within our research group. On the 30th of April, “Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers” was published on arXiv. The authors of this paper are Assistant Professor Chiheb Ben Hammouda of Utrecht University, PhD student Michael Samet of RWTH, and PI Raul Tempone. We would like to congratulate these authors on the preprint of their paper. Our research develops a data-driven continuous-time stochastic optimal control framework for intraday electricity trading by

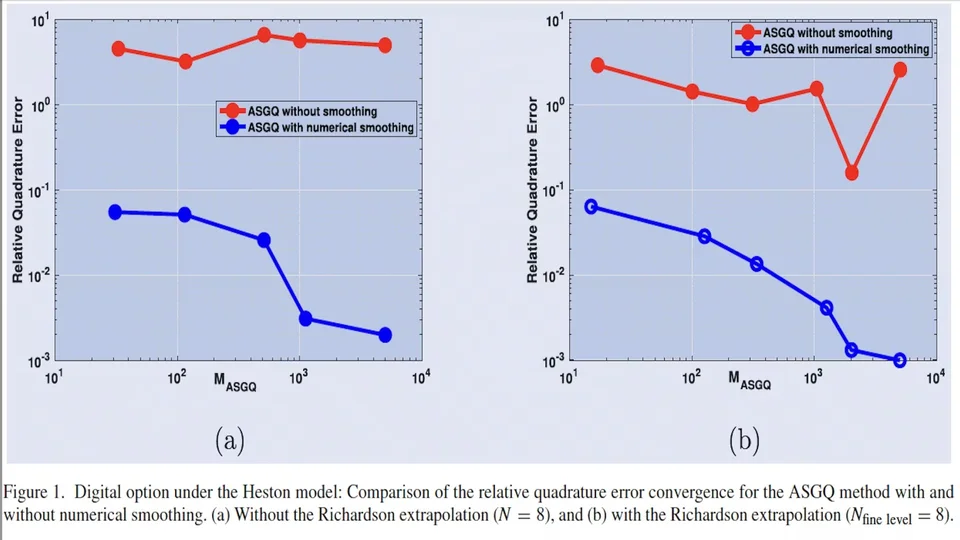

New publication in Quantitative Finance Journal 1 min read · Wed, Nov 2 2022 News Adaptive sparse grid quadrature Quasi-Monte Carlo Numerical smoothing Richardson extrapolation option pricing Monte Carlo Distribution functions Greeks Risk estimation At the end of October, the paper Numerical smoothing with hierarchical adaptive sparse grids and quasi-Monte Carlo methods for efficient option pricing by Christian Bayer ( Weierstrass Institute for Applied Analysis and Stochastics - WIAS) , Chiheb Ben Hammouda ( RWTH Aachen University ) , and Raul Tempone ( King Abdullah University of Science and Technology - KAUST; RWTH Aachen University ), was published in the Quantitative Finance Journal and is available at Taylor & Francis Online. Abstract: When approximating the expectations of a functional of a solution to a stochastic differential

Ph.D. student Eliza Rezvanova visited RWTH Aachen University 1 min read · Sun, Aug 28 2022 News During two weeks in August 2022, Ph.D. student Eliza Rezvanova visited RWTH Aachen University to collaborate with Dr. Chiheb Ben Hammouda on stochastic optimal control of renewable energy project.

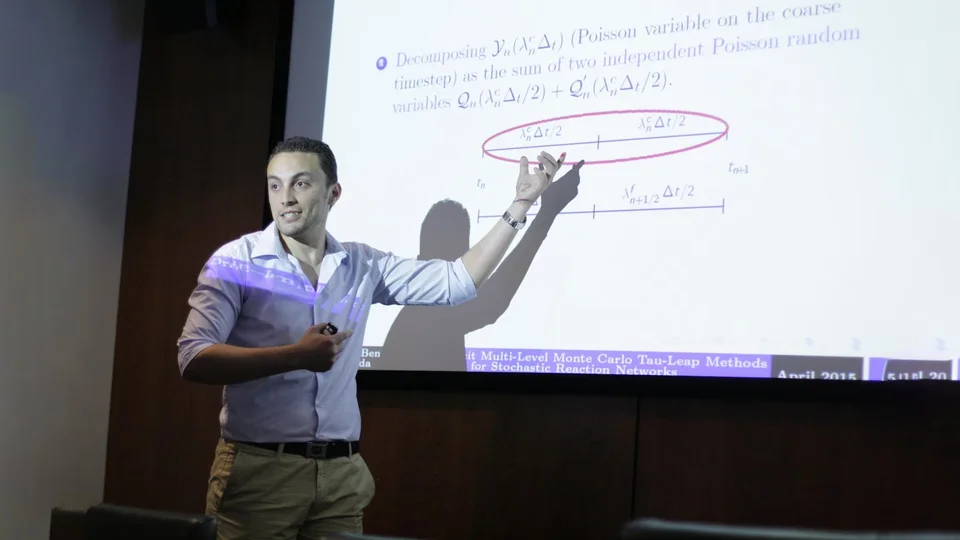

A talk by Dr. Chiheb Ben Hammouda in the Monte Carlo & Quasi-Monte Carlo (MCQMC) Methods in Scientific Computing Conference, in August 2020, University of Oxford 1 min read · Tue, Aug 11 2020 News Monte Carlo markov chains Dr. Chiheb Ben Hammouda gave, on August 11, 2020, a talk entitled "Importance sampling for a robust and efficient multilevel Monte Carlo estimator for stochastic reaction networks" in the Monte Carlo & Quasi-Monte Carlo (MCQMC) Methods in Scientific Computing Conference, 10-14 August 2020, University of Oxford.

Prof. Raul Tempone and Dr. Chiheb Ben Hammouda are organizing a minisymposia "Hierarchical Methods for Variance Reduction" at the MCQMC Conference, 10-14 August 2020, University of Oxford 1 min read · Mon, Aug 3 2020 News Monte carlo methods Prof. Raul Tempone and Dr. Chiheb Ben Hammouda are organizing a mini-symposia "Hierarchical Methods for Variance Reduction" at the Monte Carlo & Quasi-Monte Carlo Methods in Scientific Computing Conference, 10-14 August 2020, University of Oxford.

Chiheb Ben Hammouda succesfully defended his PhD Thesis 2 min read · Thu, Jul 2 2020 News On July 2nd, 2020, Chiheb Ben Hammouda successfully defended his Ph.D. thesis entitled "Hierarchical Approximation Methods for Option Pricing and Stochastic Reaction Networks"

PhD Thesis Defense: Hierarchical Approximation Methods for Option Pricing and Stochastic Reaction Networks by Chiheb Ben Hammouda 3 min read · Sun, Jun 21 2020 News In biochemically reactive systems with small copy numbers of one or more reactant molecules, stochastic effects dominate the dynamics. In the first part of this thesis, we design novel efficient simulation techniques for a reliable and robust estimation of various statistical quantities for stochastic biological and chemical systems under the framework of Stochastic Reaction Networks (SRNs).

A series of seminar talks at RWTH Aachen University (Germany) by Chiheb Ben Hammouda 1 min read · Mon, Feb 10 2020 News Chiheb Ben Hammouda will give a series of seminar talks at RWTH Aachen University (Germany) between 14 and 27 February. The talks will be related to the following manuscripts Bayer, Christian, Chiheb Ben Hammouda, and Raul Tempone. "Hierarchical adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model." Quantitative Finance Journal (2020), DOI: 10.1080/14697688.2020.1744700.

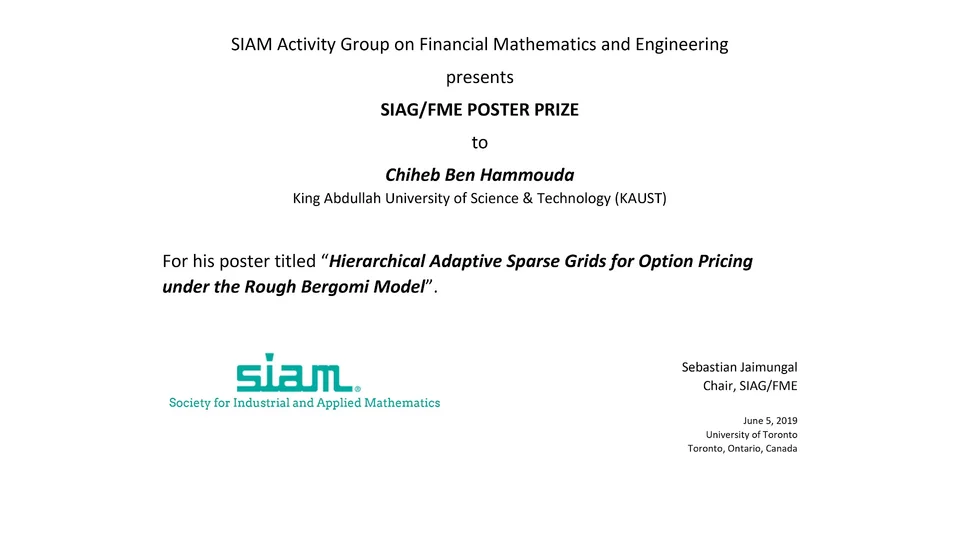

KAUST Ph.D. student wins Society for Industrial and Applied Mathematics award 2 min read · Wed, Aug 21 2019 News Spotlight Stochastic Modeling Quantitative finance Numerical simulation and analysis Chiheb Ben Hammouda, a KAUST Ph.D. student in the University's Stochastic Numerics Research Group, recently won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) held at the University of Toronto from June 4 to 7. His winning poster, titled "Hierarchical adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model," is one of several research projects carried out by Ben Hammouda under the supervision of KAUST Professor Raul Tempone.

A talk by Chiheb Ben Hammouda in the International Conference on Computational Finance 2019 (ICCF2019), Coruña, Spain 1 min read · Mon, Jul 1 2019 News Chiheb Ben Hammouda will give, on July 12, 2019, a talk entitled "Adaptive sparse grids and quasi-Monte Carlo for option pricing under the rough Bergomi model" at the International Conference on Computational Finance 2019 (ICCF2019), Coruña, Spain.

Chiheb Ben Hammouda won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) 1 min read · Thu, Jun 6 2019 News Chiheb Ben Hammouda won the best poster award at the Society for Industrial and Applied Mathematics (SIAM) Conference on Financial Mathematics & Engineering (FM19) held at the University of Toronto from June 4 to 7, 2019.

Chiheb Ben Hammouda successfully defended his MS Thesis 2 min read · Mon, May 4 2015 News On April 30th, 2015, Chiheb Ben Hammouda successfully defended his MS Thesis entitled "Drift-Implicit Multi-Level Monte Carlo Tau-Leap Methods for Stochastic Reaction Networks".

Engage ORCID ShareClipboard Related Sites Stochastic Numerics Research Group (STOCHNUM) Applied Mathematics and Computational Science (AMCS) Related Content Articles 12 Events 1 Related Links Publications on ORCID Also view Publications in the KAUST Repository LinkedIn Profile