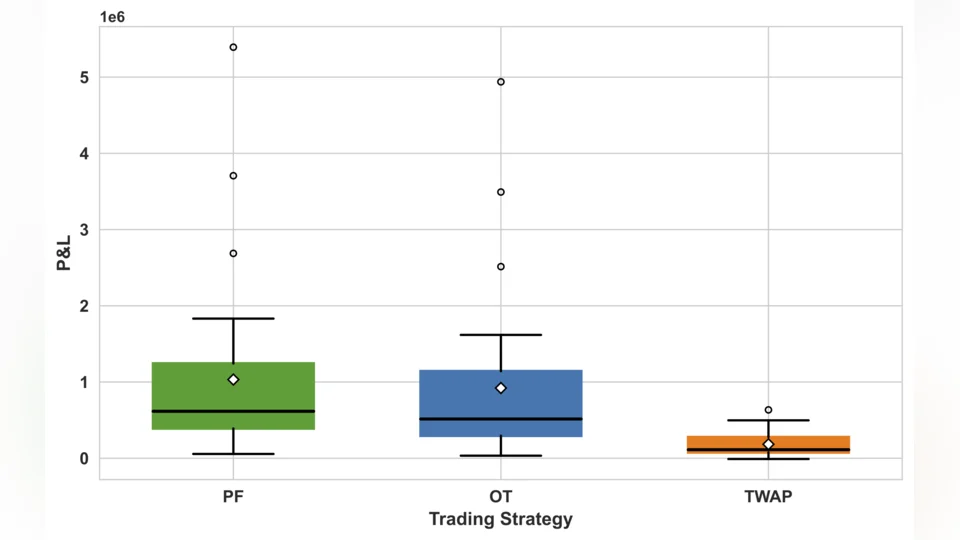

About Michael Samet Michael Samet Ph.D. Student, Applied Mathematics and Computational Science Michael Samet is a Ms/PhD Student at Stochastic Numerics Research Group (STOCHNUM) under the supervision of Professor Raul F. Tempone at King Abdullah University of Science and Technology (KAUST). Research Interests Michael's research interests include Numerical Analysis, Computational Finance, Uncertainty Quantification. Education Profile Master of Science in Applied Mathematics and Computational Sciences, King Abdullah University of Science and Technology (KAUST), Thuwal, Saudi Arabia, (January 2022 - Present). National Engineering Diploma in Multidisciplinary Engineering, École Articles Related News May 2026 Preprint in Mathematical Finance from our research team 2 min read · Mon, May 18 2026 News The Stochastic Numerics Group would like to highlight the recent achievement within our research group. On the 30th of April, “Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers” was published on arXiv. The authors of this paper are Assistant Professor Chiheb Ben Hammouda of Utrecht University, PhD student Michael Samet of RWTH, and PI Raul Tempone. We would like to congratulate these authors on the preprint of their paper. Our research develops a data-driven continuous-time stochastic optimal control framework for intraday electricity trading by December 2023 StochNum student Michael Samet achieved his Master's degree 1 min read · Wed, Dec 20 2023 News With immense pride, I dedicate this notable achievement to my cherished family, close friends, esteemed research collaborators, and the instructors from my past, all of whom have been pillars of support and encouragement throughout my transformative journey at KAUST. Particularly, I want to express my deepest gratitude to my academic advisor, Prof. Raùl Tempone, and my mentor, Prof. Chiheb Ben Hammouda, for their invaluable guidance during my MSc. studies and my wife, Hela, for her enduring patience and unwavering support. KAUST stands as a unique academic haven, fostering growth in an August 2023 Stochnum PhD Student Michael Samet participation at SIAM Conference on Financial Mathematics and Engineering (FM23) 1 min read · Tue, Aug 1 2023 News The recently concluded SIAM Conference on Financial Mathematics and Engineering (FM23) witnessed a presentation by a PhD student of our group, Michael Samet, on Quasi-Monte Carlo for Efficient Fourier Pricing of Multi-Asset Options in Lévy Models . The Conference held at Philadelphia, Pennsylvania, U.S. , between June 6-9, 2023. Abstract : High-dimensional option pricing using Fourier-based approaches is still active area of intensive research. When the expression of characteristic function is available, carefully designed Fourier pricing methods are prominent because they profit from high July 2023 Michael Samet successfully defended his MSc thesis 2 min read · Mon, Jul 31 2023 News In a remarkable display of academic excellence, On July 11, 2023, Michael Samet successfully defended his Msc. thesis entitled " Hierarchical Adaptive Quadrature and Quasi-Monte Carlo for Efficient Fourier Pricing of Multi-Asset Options Committee Chairperson: Prof. Raúl Tempone, AMCS, KAUST Committee Members: Prof . Diogo Gomes, AMCS, KAUST Prof. Mohamed-Slim Alouini, AMCS, KAUST Abstract: Efficiently pricing multi-asset options is a challenging problem in computational finance. Although classical Fourier methods are extremely fast in pricing single asset options, maintaining the tractability January 2023 Dr. Hammouda (RWTH) visits KAUST to collaborate with the StochNum Research Group 1 min read · Thu, Jan 26 2023 News Between the 10th and 24th of January, 2023, the StochNum Research Group hosted Dr. Chiheb Ben Hammouda, a postdoctoral fellow at the Alexander von Humboldt Mathematics for Uncertainty Quantification Chair in RWTH-Aachen/Germany, and a former Ph.D. student of Professor Raul Tempone at KAUST. During his visit, Dr. Hammouda, in collaboration with Prof. Tempone, worked directly with the group's students and researchers. With MS/Ph.D. student Michael Samet, they worked on a new project on developing new Fourier techniques for pricing financial derivatives and risk management. He also collaborated

Preprint in Mathematical Finance from our research team 2 min read · Mon, May 18 2026 News The Stochastic Numerics Group would like to highlight the recent achievement within our research group. On the 30th of April, “Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers” was published on arXiv. The authors of this paper are Assistant Professor Chiheb Ben Hammouda of Utrecht University, PhD student Michael Samet of RWTH, and PI Raul Tempone. We would like to congratulate these authors on the preprint of their paper. Our research develops a data-driven continuous-time stochastic optimal control framework for intraday electricity trading by

StochNum student Michael Samet achieved his Master's degree 1 min read · Wed, Dec 20 2023 News With immense pride, I dedicate this notable achievement to my cherished family, close friends, esteemed research collaborators, and the instructors from my past, all of whom have been pillars of support and encouragement throughout my transformative journey at KAUST. Particularly, I want to express my deepest gratitude to my academic advisor, Prof. Raùl Tempone, and my mentor, Prof. Chiheb Ben Hammouda, for their invaluable guidance during my MSc. studies and my wife, Hela, for her enduring patience and unwavering support. KAUST stands as a unique academic haven, fostering growth in an

Stochnum PhD Student Michael Samet participation at SIAM Conference on Financial Mathematics and Engineering (FM23) 1 min read · Tue, Aug 1 2023 News The recently concluded SIAM Conference on Financial Mathematics and Engineering (FM23) witnessed a presentation by a PhD student of our group, Michael Samet, on Quasi-Monte Carlo for Efficient Fourier Pricing of Multi-Asset Options in Lévy Models . The Conference held at Philadelphia, Pennsylvania, U.S. , between June 6-9, 2023. Abstract : High-dimensional option pricing using Fourier-based approaches is still active area of intensive research. When the expression of characteristic function is available, carefully designed Fourier pricing methods are prominent because they profit from high

Michael Samet successfully defended his MSc thesis 2 min read · Mon, Jul 31 2023 News In a remarkable display of academic excellence, On July 11, 2023, Michael Samet successfully defended his Msc. thesis entitled " Hierarchical Adaptive Quadrature and Quasi-Monte Carlo for Efficient Fourier Pricing of Multi-Asset Options Committee Chairperson: Prof. Raúl Tempone, AMCS, KAUST Committee Members: Prof . Diogo Gomes, AMCS, KAUST Prof. Mohamed-Slim Alouini, AMCS, KAUST Abstract: Efficiently pricing multi-asset options is a challenging problem in computational finance. Although classical Fourier methods are extremely fast in pricing single asset options, maintaining the tractability

Dr. Hammouda (RWTH) visits KAUST to collaborate with the StochNum Research Group 1 min read · Thu, Jan 26 2023 News Between the 10th and 24th of January, 2023, the StochNum Research Group hosted Dr. Chiheb Ben Hammouda, a postdoctoral fellow at the Alexander von Humboldt Mathematics for Uncertainty Quantification Chair in RWTH-Aachen/Germany, and a former Ph.D. student of Professor Raul Tempone at KAUST. During his visit, Dr. Hammouda, in collaboration with Prof. Tempone, worked directly with the group's students and researchers. With MS/Ph.D. student Michael Samet, they worked on a new project on developing new Fourier techniques for pricing financial derivatives and risk management. He also collaborated

Related Sites Stochastic Numerics Research Group (STOCHNUM) Applied Mathematics and Computational Science (AMCS) Related Content Articles 5 Related Links Michael Samet's publication list per year http://www.linkedin.com/in/michael-samet-531286182